Are you ready to take your small business to the next level but need extra funds to make it happen? Getting the right business loan can be the key that unlocks new opportunities and helps your business grow faster.

Whether you want to expand, buy equipment, or manage cash flow, understanding how a business loan works for small businesses can save you time and money. Keep reading to discover simple, practical tips that will help you find the best loan option tailored just for you and your business goals.

Credit: avonriverventures.com

Benefits Of Business Loans

Business loans help small businesses grow faster. They provide money to buy new equipment needed for work. This lets businesses improve quality and produce more.

Loans also help with managing cash flow. This means businesses can pay bills on time, even if money is slow to come in. It keeps the business running smoothly without delays.

Using a loan to invest in equipment can make work easier and faster. New tools help workers do better jobs and save time. This can lead to higher profits over time.

Building business credit is another big benefit. Paying back loans on time shows banks the business is trustworthy. This helps get better loans in the future with lower interest rates.

Types Of Small Business Loans

Term loans give a fixed amount of money upfront. You repay it with interest over a set time. Good for buying equipment or expanding your business.

SBA loans are backed by the U.S. government. They usually have lower interest and longer repayment terms. These loans help small businesses that need affordable financing.

Business lines of credit work like a credit card. You borrow what you need, up to a limit, and pay interest only on what you use. Flexible and useful for day-to-day expenses.

Invoice financing lets you borrow money based on unpaid invoices. It helps improve cash flow when customers delay payments. You get money quickly without waiting for invoices to be paid.

Eligibility Criteria

Credit score plays a big role in loan approval. Lenders prefer scores above 650. A higher score means better chances.

Businesses usually need to be at least 1-2 years old. Stable revenue shows ability to repay. Monthly or yearly income is checked closely.

Collateral may be required. This can be property, equipment, or inventory. Collateral lowers lender risk.

Important documents include business plans, tax returns, bank statements, and ID proofs. Clear paperwork speeds up the process.

Application Process

Preparing your business plan helps lenders understand your goals. Include clear details about your products, target market, and how you plan to use the loan. A strong plan shows you know your business well.

Gathering financial documents is key. Collect recent bank statements, tax returns, and profit and loss reports. These papers prove your business is stable and can repay the loan. Keep everything organized.

Choosing the right lender matters. Compare interest rates, fees, and loan terms from banks, credit unions, and online lenders. Pick the one that fits your needs and budget best.

Submitting the application requires care. Fill out all forms clearly and attach requested documents. Double-check for errors before sending. Being thorough speeds up approval.

Tips For Approval

Improving creditworthiness means paying bills on time and reducing debt. A higher credit score helps lenders trust you more. Keep credit card balances low and fix any errors on your credit report.

Demonstrating repayment ability shows lenders you can pay back the loan. Show steady income and keep your expenses low. Provide proof of business profits and personal savings.

Maintaining accurate records helps lenders see your business health. Keep clear records of sales, expenses, and taxes. Organized papers make the loan process faster and easier.

Seeking professional advice gives you expert help. Accountants or loan advisors can guide you through the steps. Their tips improve your chances of loan approval.

Credit: cumberlandbusiness.com

Common Challenges And Solutions

Loan rejections happen often for small businesses. Common reasons include poor credit scores, lack of financial history, or incomplete applications. Staying calm and asking for feedback helps improve future applications. Consider working with a financial advisor or improving your business plan before reapplying.

Managing loan repayments requires a clear plan. Set a budget that covers monthly payments without stress. Prioritize paying on time to avoid late fees and maintain a good credit score. Automatic payments can simplify the process and reduce missed payments.

Avoiding debt traps means borrowing only what you can repay. Watch out for high-interest rates and hidden fees. Choose loans with clear terms and avoid adding more debt to cover old loans. Keep track of all debts and payments in one place for easy management.

Alternative Funding Options

Crowdfunding lets many people give small amounts of money. It works well for new ideas or products. Success depends on good marketing and a clear plan.

Angel Investors are wealthy people who invest in small businesses. They offer money and advice but may want part ownership. Trust and clear agreements are important.

Grants and Subsidies are funds from governments or groups. These do not need to be paid back. Rules and eligibility vary, so check carefully.

Peer-to-Peer Lending connects borrowers directly with lenders online. Interest rates can be lower than banks. It requires a good credit score and a strong plan.

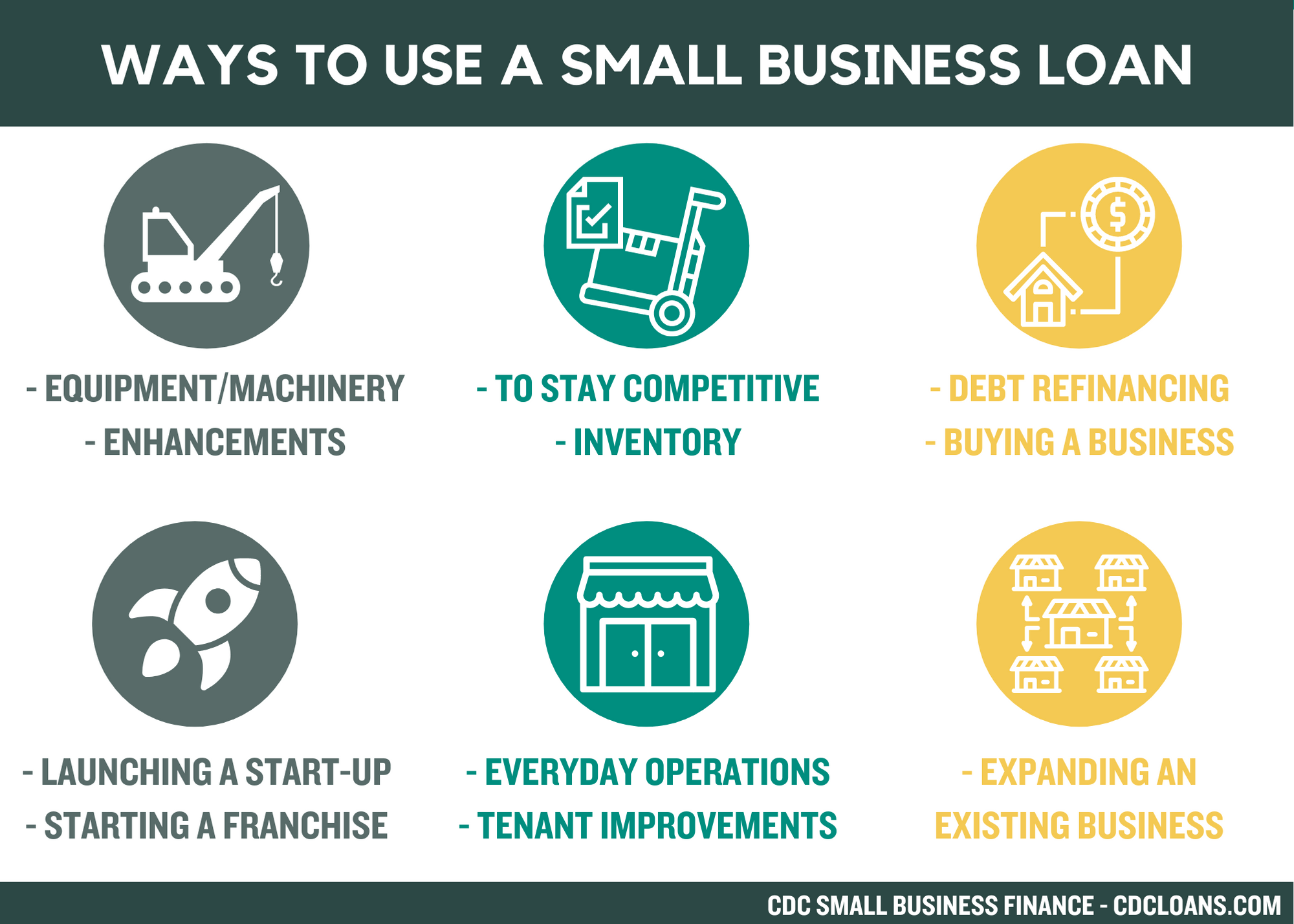

Credit: cdcloans.com

Frequently Asked Questions

What Qualifies A Business For A Small Business Loan?

Small businesses must show steady revenue, a good credit score, and a solid business plan. Lenders also consider industry type and loan purpose. Meeting these criteria improves loan approval chances.

How Can I Improve My Small Business Loan Approval?

Improve credit score, prepare a clear business plan, and show consistent cash flow. Providing collateral or a personal guarantee can also help secure approval faster.

What Types Of Loans Are Best For Small Businesses?

Term loans, SBA loans, and lines of credit are popular. Choose based on your funding needs, repayment ability, and loan terms. Each type serves different business purposes.

How Long Does It Take To Get A Small Business Loan?

Approval time varies from a few days to several weeks. Online lenders are faster, while traditional banks may take longer due to thorough reviews.

Conclusion

Getting a business loan can help small businesses grow and succeed. It provides the money needed for equipment, staff, or new projects. Understanding loan options and terms is very important. Choose the loan that fits your needs best. Manage your loan wisely to avoid problems.

A good loan can support your business goals. Take time to plan before applying. Success often starts with smart financial choices.